IC Insights released the August update of the 2019 McLean report earlier this month. This update includes the first part of an in-depth analysis of the Foundry industry, the latest forecast for semiconductor capital expenditures this year, and the top 25 1H19 semiconductor suppliers and their 3Q19 sales prospects.

Below, we will specifically introduce the revenue of the top 15 semiconductor manufacturers in the global rankings in the first half of this year.

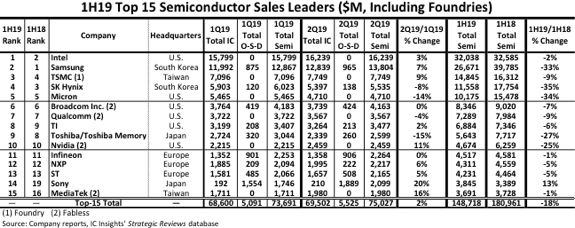

As shown below, the top 15 semiconductor manufacturers (IC and OSD optoelectronics, sensors and discrete devices) have sales rankings, including six US-based suppliers, three in Europe, two in Taiwan, and South Korea. And Japan.

Since Samsung took the lead in the second quarter of 2017, in the first half of this year, Intel replaced Samsung and returned to the leader position. Although Samsung ranked first in 2017 and 2018, it is expected that Intel will easily regain the top position in 2019, which is the company's position from 1993 to 2016.

With the collapse of the DRAM and NAND markets, the storage market has undergone a complete transformation in the past year. In the first half of 2018, Samsung's total semiconductor sales were 22% higher than Intel's, but by the first half of 2019, the situation had turned around, and Intel's semiconductor sales were 20% more than Samsung's!

Compared with the first half of 2018, the sales of the top 15 semiconductor companies in the same period of this year fell by 18%, while the global semiconductor industry's overall decline in the first half of the year was 14%. Three major memory suppliers - Samsung, SK Hynix and Micron - With each company's annual growth of more than 36%, revenue in the first half of 2019 fell by at least 33% year-on-year, indicating the extreme instability of the memory market. Nine of the top 15 companies had sales of at least $5 billion in the first half of the year, compared to the first half of 2018, with one company missing. As shown, the bottom line for the 15 largest semiconductor suppliers in the first half of 2019 was about $3.7 billion.

Compared with the first half of 2018, there are two new ones entering the top 15. Fabless IC supplier MediaTek rose from 16th to 15th. IDM Sony is the only supplier in the top 15 growth in the same period last year. It rose 5 places in the first half of the year and became the 14th largest. Semiconductor supplier. As shown, 90% of Sony's semiconductor sales come from OSD devices, mainly image sensor components for smartphones.

The top 15 in the first half of this year included a pure wafer foundry (TSMC) and four fabless companies. If TSMC is excluded from the rankings, China's fabless IC supplier HiSilicon ($3.5 billion) will be ranked 15th. Compared with the first half of 2018, Haisi's sales in the first half of this year increased by 25%. However, since more than 90% of Hisilicon's IC sales are internal to Huawei, Huawei's “blacklist” in the US government may slow down the sales growth rate of HiSilicon in the second half of this year.

IC Insights' top 15 semiconductor supplier rankings include wafer foundries because it has consistently ranked this ranking as the best supplier list, not market share ranking, and realized that in some cases semiconductor sales are double counting of. Many of their customers are suppliers to the semiconductor industry (semiconductor equipment, chemicals, gases, etc.), and large IC manufacturers, excluding wafer foundries, will leave significant “holes” in the list of top semiconductor suppliers.

As shown, the latest top 15 lists can be used as a reference to determine which companies are major semiconductor suppliers, whether they are IDMs, fabless companies or foundries.

Many major semiconductor companies have provided sales guidance for the third quarter of 2019, which is discussed in more detail in the August update. Overall, the 3Q19 / 2Q19 revenue growth expectations of the top 25 major semiconductor suppliers vary from company to company and currently range from + 21% to -2%.